Investment returns depend partly on what is held and partly on where it is held. Two portfolios with identical underlying assets can produce different after-tax outcomes when those assets are assigned to different account types. The practice of making that assignment deliberately — routing each investment type toward the account where its tax treatment is most favorable — is called asset location. The concept is distinct from asset allocation (how much of each asset class to hold) and applies specifically to investors who maintain both taxable brokerage accounts and tax-advantaged retirement accounts simultaneously.

What is asset location, and why does the account type matter for tax treatment?

What is asset location, and why does holding the same investment in a taxable account versus a tax-advantaged account produce different tax outcomes?

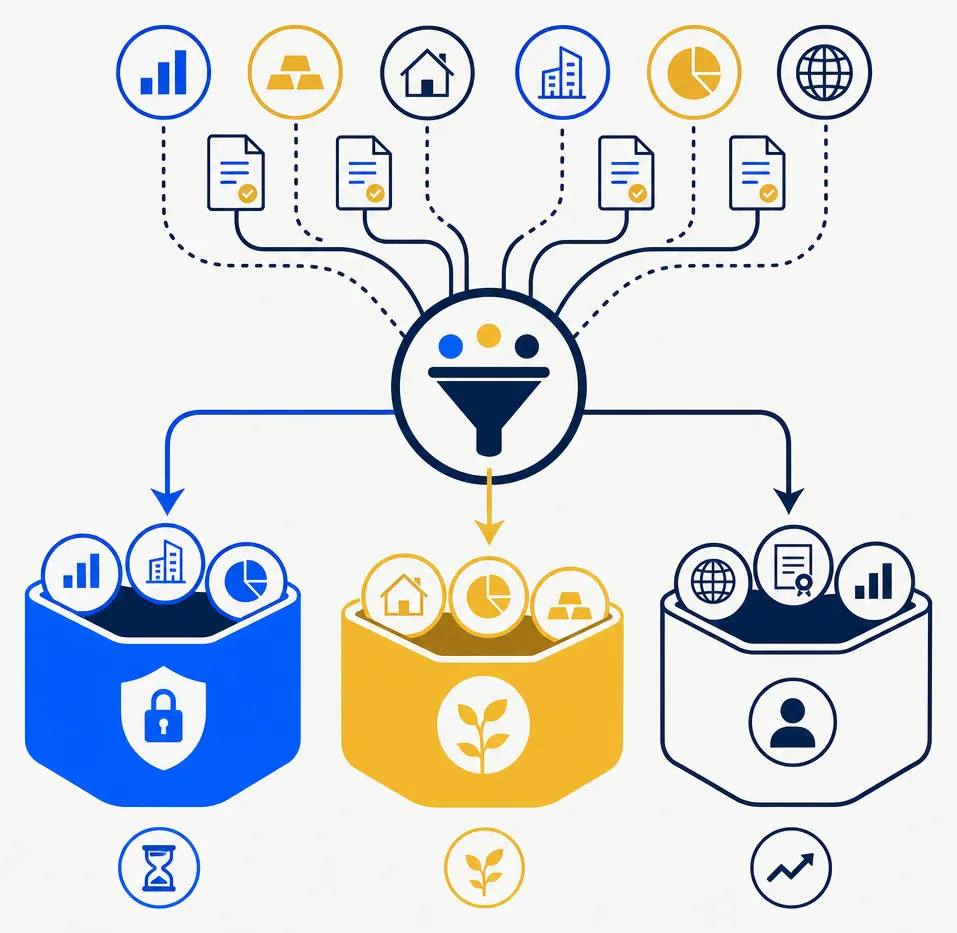

Asset location is the practice of assigning specific investments to specific account types — taxable brokerage, traditional IRA or 401(k), or Roth IRA — based on each investment's tax-distribution profile, because the same return is taxed differently depending on the account that generates it: a bond paying ordinary-rate interest inside a tax-deferred account creates no current-year tax event, while the same bond in a taxable account may generate an annual tax liability even when the investor makes no trades.

The mechanism is structural. In a taxable brokerage account, income events — dividends, interest payments, and capital gain distributions — generate current-year tax liability in the year they are received, at rates that depend on character and holding period. In a traditional tax-deferred account such as a 401(k) or traditional IRA, returns compound without current-year taxation, and the tax event is deferred until withdrawal, at which point distributions are taxed as ordinary income. In a Roth account, qualified withdrawals are potentially tax-free entirely, making Roth a structurally distinct third option where the compounding itself may occur in a tax-exempt environment.

The location optimization opportunity arises from this structural difference. An investment with high expected ordinary-income distributions creates ongoing annual tax drag in a taxable account but none inside a tax-deferred account. Moving that investment to the deferred account — and placing a comparably valued tax-efficient investment in the taxable account — may reduce annual tax drag without altering the portfolio's overall allocation to each asset class. The ETF vs mutual fund tax efficiency article covers how vehicle choice affects an equity investment's income-distribution profile — an important input to location decisions for the equity portion of a portfolio.

Which types of investments tend to create the most tax drag in a taxable account?

What investment types are typically considered most tax-inefficient when held in a taxable brokerage account?

Investments generating high levels of ordinary income — taxable bonds paying regular interest, actively managed funds with frequent portfolio turnover and large annual capital gain distributions, and real estate investment trusts whose distributions are primarily ordinary income — tend to create the most ongoing annual tax drag in a taxable account, because ordinary income rates may be significantly higher than the preferential long-term capital gains rate applicable to qualified dividends and long-term appreciation.

The character of the income matters as much as its size. Ordinary interest income from most taxable bonds may be taxed at rates up to approximately 37% under current law for high-income investors, while qualified dividends and long-term capital gains may qualify for preferential rates that are potentially lower — historically often approximately 15% or approximately 20% for higher-income investors. An active equity fund that generates frequent short-term capital gain distributions from portfolio turnover can produce taxable income that is effectively treated as ordinary income by shareholders in a taxable account, even in years when the investor made no redemptions.

High-turnover funds of any kind create larger annual tax events in taxable accounts. A fund that restructures its portfolio frequently recognizes gains internally and distributes them to shareholders, often in December. Shareholders in a taxable account owe tax on those distributions in the year received, regardless of whether they sold any shares of the fund or held through the distribution date by coincidence. The same fund inside a tax-deferred account produces no current-year event from the distribution. The rebalancing and account-type article explores how this principle — that the account determines the tax consequence more than the specific trade — applies to rebalancing decisions across multiple account types.

What types of investments tend to fit naturally in tax-advantaged accounts?

What investment types are commonly placed in tax-deferred or Roth accounts to shelter their tax-inefficient income characteristics from current taxation?

Taxable bonds, high-turnover active equity funds, and REITs generating primarily ordinary-income distributions are commonly placed in tax-deferred accounts where their annual distributions compound without current-year taxation; Roth accounts are often prioritized for assets with the highest expected long-run growth, since qualified withdrawals are potentially tax-free and the compounding benefit inside a Roth may be larger than the same compounding inside a taxable account taxed annually on distributions.

The conventional heuristic — place bonds in the IRA, hold broad equity exposure in the taxable account — reflects a straightforward observation: bond interest is typically ordinary income, while a broad-market equity index ETF may generate a relatively low annual income distribution, much of it potentially qualified, compared with a taxable bond fund holding comparable notional value. The ordinary interest income from most bond funds is taxed each year at full ordinary income rates, regardless of whether the bonds themselves were sold or matured.

Roth accounts add a forward-looking dimension to the decision. Because Roth growth compounds potentially without future taxation on qualified distributions, assets placed in a Roth earlier in an investor's holding period may benefit most from that structure over a long horizon. For investors coordinating Roth conversions with capital-gain recognition decisions in a given tax year, the interaction between conversion income, bracket position, and capital loss offsets can affect how much conversion is efficient in that year. The Roth conversions and TLH article covers how conversion income interacts with harvested losses and bracket management in the same tax year.

How does a direct-index tax-loss harvesting sleeve change the asset-location approach?

Does running a direct-index tax-loss harvesting program in a taxable account change which assets belong there versus in a tax-advantaged account?

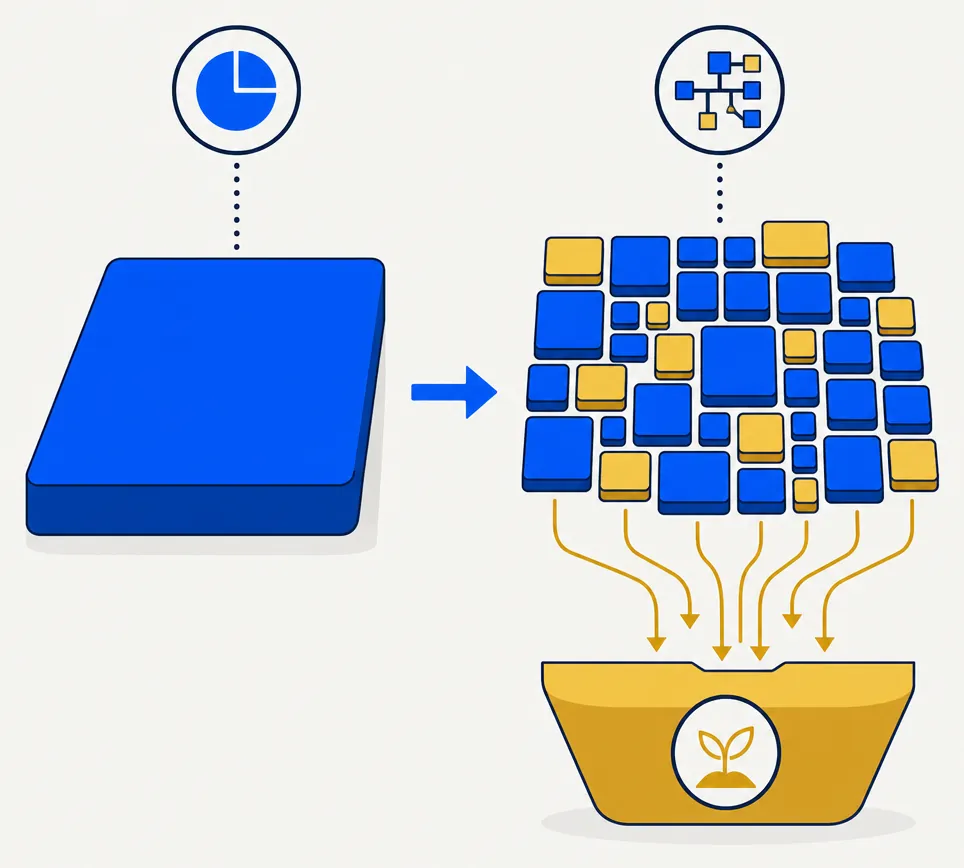

A direct-index TLH sleeve in a taxable account transforms the location calculus meaningfully: rather than treating the taxable account as a residual venue for whatever remains after filling tax-advantaged space, the TLH program may make the taxable account an active tax-generation engine that produces a stream of realized losses — potentially offsetting gains from rebalancing, Roth conversions, or concentrated-stock exits — making granular equity exposure in the taxable account strategically valuable rather than merely tolerable.

The conventional asset-location framework was developed largely in the context of passive ETF portfolios, where the taxable account is treated as a residual: the most tax-inefficient assets go to deferred accounts first, and the taxable account absorbs what remains. A direct-index sleeve changes part of this logic. By holding a diversified set of individual equities in the taxable account rather than a single ETF, the portfolio gains granular harvest surface: the ability to realize losses on individual securities while maintaining market exposure through replacement securities. A single-ETF equity position generates one loss opportunity when it declines; many individual positions may generate many independent loss opportunities simultaneously across different market conditions.

Harvest activity in the direct-index sleeve can produce a stream of capital losses that carry forward indefinitely under IRC §1212. That loss reserve may offset gains from rebalancing other parts of the portfolio, from Roth conversions, or from concentrated-stock liquidation events — in years beyond the one in which the loss was originally realized. The TLH vs ETF rebalancing article covers the structural difference in harvest surface between a single-ETF position and a direct-index sleeve. The direct indexing in 2026 article covers fit criteria and account-size thresholds for adding this structure.

HarvestEngine's portfolio decomposition separates each account's holdings into the beta

sleeve (passive broad-market ETFs), the long direct-index sleeve, and the optional short

overlay. The long sleeve is explicitly designed for the taxable account, where its harvest

activity may generate real tax value that compounds into a loss reserve over time

(src/tlh/portfolio/decomposition.py).

What practical constraints limit perfect asset-location optimization?

What are the real-world constraints that prevent investors from achieving a theoretically optimal asset location across their accounts?

Contribution limits restrict how much can be added to tax-advantaged accounts each year, employer-plan menus limit which funds are available inside a 401(k), embedded gains in taxable positions cannot be relocated without triggering immediate taxation, and the coordination overhead of rebalancing across multiple accounts adds meaningful operational friction — making asset location an incremental direction to apply gradually rather than a binary state achievable all at once.

The most immediate constraint is that tax-advantaged accounts accept only new contributions up to annual statutory limits. An investor who wants to move a large taxable bond position into a deferred account cannot transfer the securities directly — they can only add incrementally through new annual contributions or by selling the taxable position (potentially triggering a gain or loss event) and directing new cash to the deferred account over multiple years. For large portfolios, the math on full relocation over the allowed annual contribution window may span more than a decade.

Embedded gains create an additional friction. Appreciated positions in a taxable account cannot be relocated without recognizing the embedded gain. For a position with a substantial unrealized gain, the tax cost of selling to relocate may exceed the ongoing annual tax drag from leaving it in place. Many investors hold historically appreciated equity positions in taxable accounts indefinitely because the relocation cost outweighs the location benefit — a judgment that may shift at retirement, estate transfer, or if charitable donation of the appreciated position becomes part of the picture. The tax alpha article covers how these multi-year routing decisions compound into meaningful after-tax differences over a full investment horizon, framing why incremental improvement toward better location may be worth sustained attention even when a theoretically perfect state is not achievable in a single step.

Employer plan menus further limit the optimization available inside a 401(k). An investor who wants to hold an active bond fund or international equity fund inside the deferred account may find the plan offers a limited menu at higher expense ratios than the equivalent taxable ETF alternative. When the higher fund cost in the deferred account exceeds the tax benefit of sheltering that fund's income distributions, holding the lower-cost ETF in the taxable account may be more efficient net of fees. Asset location is always a net-of-all-costs calculation, not just a gross-tax optimization.

Read this next with the 401(k) vs taxable rebalance guide, ETF tax efficiency vs mutual funds, Roth conversions and TLH, direct indexing in 2026, and tax alpha explained.