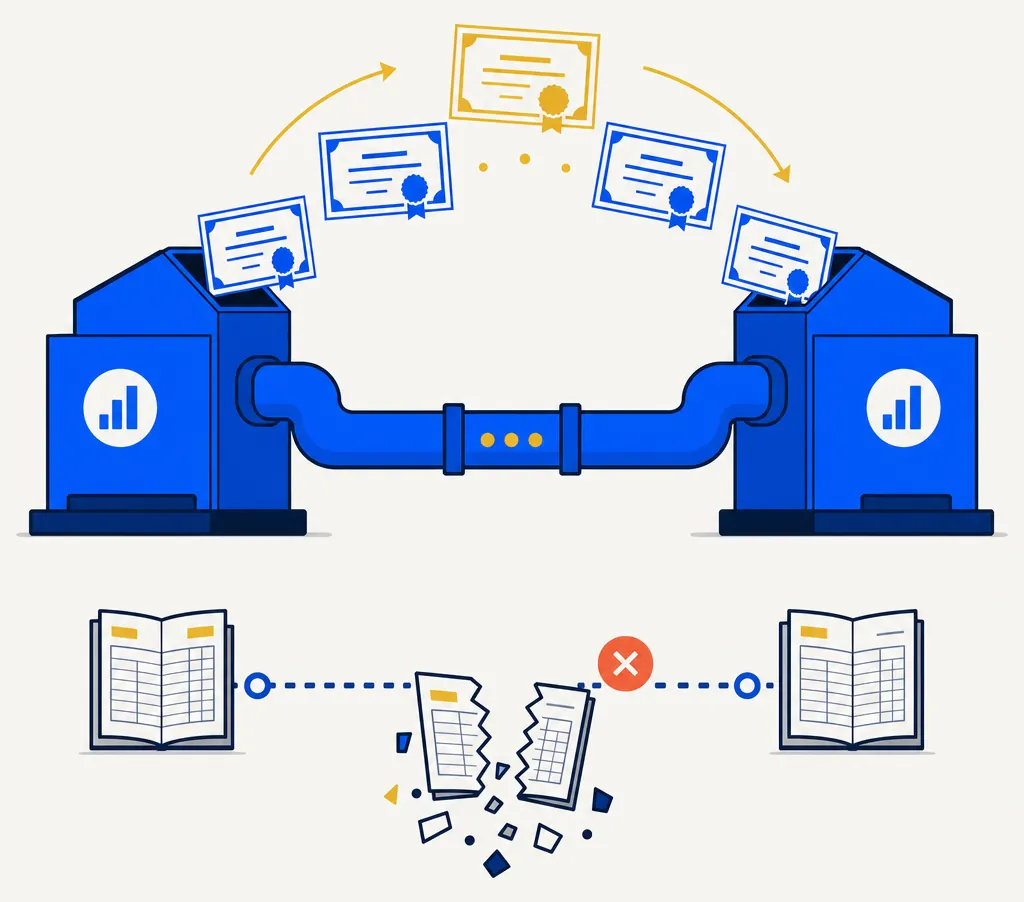

When moving a brokerage account, the shares typically transfer in-kind through the DTCC's Automated Customer Account Transfer (ACAT) system — without triggering a taxable sale event. But the cost basis records behind those shares don't always follow. In a notable share of transfers, the receiving broker inherits securities with no record of original acquisition price, acquisition date, or lot structure. Without that information, the tax math behind every future sell decision becomes unreliable — and the IRS may treat unknown basis as zero, potentially inflating the taxable gain on sale.

For investors running a tax-loss harvesting strategy, a cost-basis gap compounds quickly. Lot selection, wash-sale tracking, and harvest eligibility all depend on accurate lot-level data. Here is what happens during an ACAT transfer, why basis records go missing, and what to verify before and after initiating one.

What is an ACAT transfer?

What is an ACAT transfer, and how does it move securities between brokers without triggering a taxable sale?

An ACAT (Automated Customer Account Transfer) is a standardized, DTCC-managed process that moves securities between US broker-dealers in-kind — transferring the shares themselves rather than liquidating them — so no capital gain or loss is recognized at the time of the move under IRC §1001.

The ACAT system is operated by the Depository Trust & Clearing Corporation (DTCC) and handles the substantial majority of individual retail brokerage transfers in the United States. When an investor submits a transfer form to the receiving broker, that broker initiates the request through the ACAT system. The delivering broker typically has three business days to validate the account — confirming identity and resolving open margin calls or unsettled trades — and then transfer the positions.

The defining tax feature of an in-kind transfer is neutrality on the transfer itself. The investor does not recognize gain or loss when shares move from broker A to broker B. The holding period and cost basis carry over — at least in principle. The practical question is whether those records actually make the same trip as the shares.

Why does cost basis get lost during a transfer?

Why do cost basis records sometimes fail to transfer between brokers, even when the shares themselves move correctly?

Cost basis records travel through a separate data channel that brokers are required to transmit but may not always complete correctly — particularly for noncovered (pre-2011) lots, multiply-transferred accounts, fractional shares, or positions subject to complex corporate actions — leaving the receiving broker with "unknown basis" that may be treated as $0.

Since 2011, the IRS has required brokers to track and report cost basis on "covered" securities — broadly, stocks purchased after January 1, 2011. For these covered lots, the delivering broker is supposed to transmit basis data alongside the ACAT transfer via a supplemental DTC data message. The ACAT system itself carries only the securities and cash; basis is an auxiliary element that travels on a separate, best-effort channel.

Several conditions tend to break the basis transfer:

- Noncovered (pre-2011) lots. Securities purchased before the applicable coverage start date are "noncovered." Brokers have no regulatory obligation to report these lots' basis to the IRS or to the receiving broker. Some deliver this data voluntarily; many do not.

- Multiple prior transfers. Each ACAT hop is a fresh basis transmission. An account transferred twice — from broker A to B, then B to C — may carry basis gaps from the first hop that the intermediate broker never reconciled.

- Corporate actions, splits, and spinoffs. Mergers, stock splits, and spinoffs require basis adjustments that broker systems handle inconsistently. A lot acquired through a reorganization may arrive at the receiving broker with the pre-event basis or no basis at all.

- ESPP shares and employer plan rollovers. Employee stock purchase plan shares and employer stock transferred from a retirement plan often carry compensation-income adjustments to their tax basis. These adjustments may not transmit through standard ACAT channels.

What does "unknown basis" mean for a tax return?

What happens on a tax return when a broker reports a sale with unknown cost basis, and how does the IRS handle the gap?

When a broker cannot determine the cost basis of a sold lot, it typically reports the sale on Form 1099-B with basis listed as unknown or as $0, and the investor is responsible for reconstructing the actual basis from original purchase records — a process that can take considerable time and may still be incomplete enough to invite an IRS follow-up.

An unknown-basis 1099-B entry does not automatically produce a $0 gain — but the investor bears the reconstruction burden. The IRS's matching algorithms may flag returns where the reported gain looks unusually large relative to historical holding periods. More practically, investors who sell a position they believe carries a loss may discover that the basis their broker recorded was incorrect, meaning the harvest produced a different tax result than the portfolio software projected.

For a tax-loss harvesting strategy, the consequences are material. Lot selection — FIFO, HIFO, specific-ID — is meaningless without reliable lot-level basis data. A broker that shows a single "unknown" entry at position level cannot support per-lot sell instructions, and the harvest decision defaults to an uncontrolled, potentially tax-inefficient outcome. For a detailed look at how lot-selection methods differ, see FIFO, LIFO, HIFO, specific-ID: how lot selection changes your tax bill.

Wash-sale tracking is similarly affected. If the receiving broker doesn't know the acquisition dates for incoming lots, it cannot accurately identify whether a replacement purchase lands inside the 30-day wash-sale window. Replacement lot purchases may go unrecorded as wash events, creating apparent losses that the IRS may later disallow. The wash-sale rule depends entirely on accurate lot-level date and basis data to apply correctly.

What to verify before initiating a broker transfer

What steps are worth completing before submitting an ACAT transfer request to reduce the risk of arriving at the receiving broker with incomplete basis records?

Before submitting an ACAT transfer, investors typically benefit from downloading a complete lot-level cost-basis report from the delivering broker, identifying any noncovered or unknown-basis lots, and reconstructing original purchase records for those positions — because once the transfer completes, the delivering broker may archive or purge those records.

A practical pre-transfer checklist that many investors find useful:

- Download a full position and cost-basis report. Most brokers offer a CSV export of all lots with acquisition date, acquisition price, and covered/noncovered status. This becomes the reconstruction document if the receiving broker's import is incomplete.

- Identify noncovered positions explicitly. Filter for lots marked "noncovered" or with no basis recorded. Original brokerage confirmations, 1099-B forms from prior years, or the broker's own historical records may be the only available sources for these positions.

- Check for recent corporate actions. If any position was subject to a spinoff, merger, or stock split in the past 12 months, verifying that the basis reflects the post-event adjustment before initiating the transfer reduces the risk of arriving with a stale basis figure.

- Time the transfer to avoid open wash-sale windows. If a loss harvest was completed recently, an active 30-day wash-sale window may exist on one or more symbols. A transfer during that window does not close it — but if the receiving broker doesn't carry the window forward, a future repurchase may create an untracked wash event. See wash-sale rules across spouse accounts for the broader household-coordination picture, where IRA and spousal purchases interact with the same window.

How HarvestEngine handles accounts with transferred lots

How does HarvestEngine approach harvest eligibility when an account contains lots with incomplete or missing cost basis from a prior broker transfer?

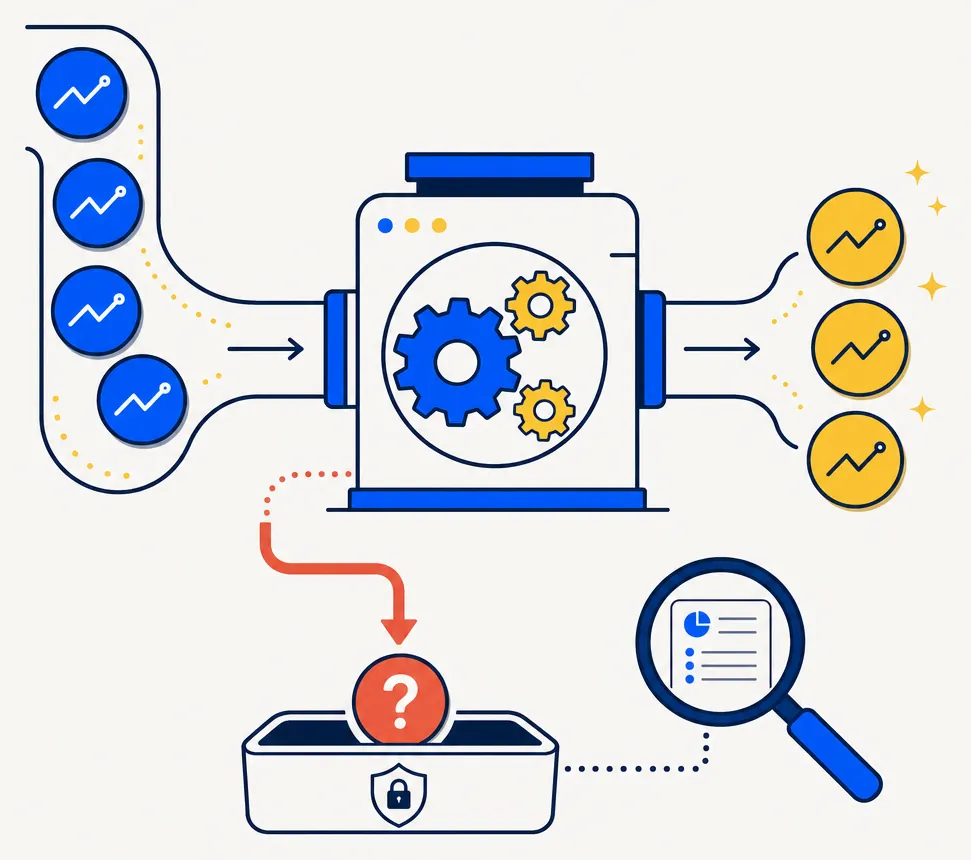

HarvestEngine excludes lots with unknown or zero cost basis from harvest candidate lists to avoid surfacing incorrect loss estimates, and surfaces those positions in the Loss Watch panel so investors can initiate corrective action before the engine considers them eligible.

When the engine syncs an account's positions from E*TRADE, it loads lot-level basis and acquisition date from the portfolio endpoint. Lots that arrive with no acquisition date or a basis of approximately $0 are tagged internally and excluded from the optimizer's harvest candidate set. During the portfolio sync, unknown-basis lots are flagged with an internal marker that the lot-selection engine recognizes and skips during candidate scoring.

The practical effect is conservative: an investor who transfers an account carrying several noncovered lots may see fewer harvest candidates than their total position count suggests. That undercount is intentional — it prevents the engine from recommending a harvest based on a basis figure that may be wrong by a material amount. Once the investor reconstructs and enters the correct basis through E*TRADE's cost-basis correction flow, those lots become eligible on the next daily sync.

For investors working through a basis reconstruction, the Form 8949 walkthrough explains how unknown-basis lots appear on the filing, and TLH 101 covers the broader harvest workflow that depends on reliable lot-level data.

Read this next with lot selection methods, the wash-sale rule demystified, the Form 8949 filing walkthrough, and TLH 101.